Paul Hudson: The Man Who Sold The Stars

Disclosure: Blue Spoon worked with Sanofi during Paul Hudson's tenure as CEO. The analysis and opinions expressed here are the author's own.

Boards don't fire CEOs for failing. They fire them for failing on schedule.

Failure itself is tolerable, sometimes even narratively useful, so long as it is random, deniable, or safely buried in a footnote. What is intolerable is failure that arrives in sync with the quarterly drumbeat. Failure that lands precisely when guidance was supposed to hold. Failure that refuses to bend itself to the earnings calendar. A failed molecule? That's science. A delayed trial? That's complexity. A strategic bet that depresses margin for three straight quarters while promising payoff in year four? That's insubordination.

Public markets don't punish failure in the abstract. They punish visible deviation from expectation. They punish the appearance of losing control. They punish the CEO who says, "This will take time," in a system engineered to hear only, "This will accrete by Q3." The modern board doesn't ask: Was the bet coherent? It asks: Can we survive the next call?

The problem isn't that experiments fail. The problem is that experiments unfold on biological timelines, while markets operate on broadcast schedules. Evolution runs in seasons. Earnings run in quarters. And when the two collide, it is always evolution that gets blamed.

Jeff Bezos essentially had to train Wall Street to accept a seven-year horizon for major initiatives, and educate investors on why free cash flow mattered more than GAAP earnings. He built an entire institutional culture around "willingness to fail, the patience to think long-term." And it worked — Amazon is now a $700 billion self-generating economic system because he had the conviction, the communication discipline, and the concentrated ownership to make the market bend to his timeline instead of the other way around.

In his book Adapt: Why Success Always Starts with Failure, Tim Hartford outlines Charles Darwin's discovery of a vast array of distinct species in the Galapagos Islands, a state of affairs that contrasts with the picture seen on large continents, where evolutionary experiments tend to get pulled back toward a sort of ecological consensus by interbreeding. "Galapagos isolation" versus the "nervous corporate hierarchy" is the contrast staked out by Hartford in assessing the ability of an organization to innovate.

On isolated islands, mutations have room to breathe, to fail, to succeed, to become something entirely new without being immediately swamped by the genetic consensus of the mainland.

But on continents — or in corporate hierarchies — firmly established ecosystems blur and swamp new adaptations before they have a chance to prove themselves. The difference isn't about the quality of the mutations. It's about whether the environment tolerates their existence long enough to find out if they work. "In large organizations," Hartford writes, "ideas are exposed too early to the antibodies of hierarchy. Committees demand proof before there is evidence, certainty before there is experience. What might have become a breakthrough is optimized into mediocrity."

The lesson is brutal in its simplicity: isolation enables innovation. Consensus kills it.

Which helps explain why Europe — with its deep capital markets, world-class universities, and highly educated workforce — can't seem to produce anything that scales beyond regional success. The continent that invented the scientific method now operates as one giant committee demanding certainty before experience. Every mutation gets pulled back to consensus before it can prove itself. The Americans build Amazon, Google, Meta, Apple, brands that reorganize entire economies. The Chinese build Alibaba, Tencent, ByteDance, brands that command billions of users. Europe's response? Regulations. The gap isn't about talent or resources. It's about whether an economic system tolerates evolutionary experiments long enough to let them work. Brussels demands proof; Silicon Valley tolerates failure. One gets paperwork. The other gets power.

Most people who work in corporations or academia have witnessed something like the following: A number of "creatives" or engineers are sitting together in a room with a big whiteboard, bouncing ideas off one another. Out of the discussion emerges a new concept that seems promising. Then some laptop-wielding person in the corner, having performed a micro-second search with ChatGPT or Gemini, announces that this "new" idea is, in fact, an old one — or at least vaguely similar — and has already been tried. (In healthcare especially, this reflex has become epidemic. Every idea has a precedent. Every precedent has a post-mortem. The verdict arrives before the experiment even begins.)

If the idea failed before, no rational manager, trained by quarterly earnings calls and career risk calculus, will fund its resurrection. Failure has already been entered into the permanent record. If it succeeded? Worse. It's patented. First-mover advantage. Barriers to entry. The market is "closed." The spreadsheet has spoken. So the room folds in on itself. The whiteboard is wiped clean. The new species dies in infancy, not because it was weak, but because it was exposed too early to the antibodies of precedent.

Millions of ideas have been crushed this way. Not by stupidity. Not by lack of capital. But by instantaneous comparison, by the tyranny of searchable history.

What if that person in the corner hadn't been able to do a Gemini or ChatGPT search?

It might have required weeks of library research to uncover evidence that the idea wasn't entirely new, but only after a long and toilsome slog through many books, tracking down many references, some relevant, some not. When the precedent was finally unearthed, it might not have seemed like such a direct precedent at all. There might be reasons why it would be worth taking a second crack at the idea, perhaps combining it with concepts and innovations from other fields. Hence the virtues of Galapagan isolation.

The counterpart to Galapagos isolation is the struggle for survival on a large continent, where firmly established (i.e., deeply embedded) ecosystems tend to blur and swamp new adaptations. Jaron Lanier — a computer scientist, composer, visual artist, Prime Unifying Scientist at Microsoft's Office of the Chief Technology Officer, and author of the book You Are Not a Gadget: A Manifesto — has some insights about the unintended consequences of the Internet, the informational equivalent of a large continent on our ability to take risks:

"In the pre-Net era, managers were forced to make decisions based on what they knew to be limited information. Today, by contrast, data flows to managers in real time from countless sources that could not even be imagined a couple of generations ago. And powerful computers organize and display the data in ways that are as far beyond the hand-drawn graph-paper plots of my youth as modern video games are to tic-tac-toe. In a world where decision makers are so close to being omniscient, it's easy to see risk as a quaint artifact of a primitive and dangerous past."

The illusion of eliminating uncertainty from corporate decision making isn't just a question of management style or personal preference. In the legal industrial complex that has developed around publicly-traded corporations generally, and the pharmaceutical industry specifically, managers are strongly discouraged from shouldering any risks that they know about, or, in the opinion of some future jury, should have known about, even if they have a hunch that the gamble might pay off in the long run.

So there is no long term in industries driven by the next quarterly report.

The possibility of some innovation making money is just that — a theory, a mere possibility that will not have time to materialize before the subpoenas from minority shareholder lawsuits (or activist investors) begin to roll in.

This is one reason why $14 billion a year in DTC advertising of prescription drugs in the United States looks identical. Not because pharma marketers lack imagination, but because the legal department won't approve anything that deviates from precedent. Innovation means liability. Consensus means safety. So you get a hundred different drugs selling themselves with the exact same story, optimized into indistinguishable mediocrity, which is just Harford's thesis playing out at thirty seconds per spot.

Today's impatience and belief in ineluctable certainty is the true innovation killer of our age. In this environment, the best an audacious manager can do is to tweak the edge, develop small improvements to existing systems, climbing the hill, as it were, toward a local maximum, locked in a feedback loop that understands and rewards trimming the fat, eking out the occasional operational improvement. This is the biggest reason why any system of markets roughly defined as healthcare — in the United States; in the United Kingdom; in Europe — can't break out of perpetual crisis and collapse.

Said another way, any strategy that involves crossing a valley, accepting short-term losses to reach a higher hill in the distance, will soon be brought to a halt by the demands of an economic system that celebrates short-term gains and tolerates stagnation, but condemns anything else as a failure. In short, a world where big stuff can never get done.

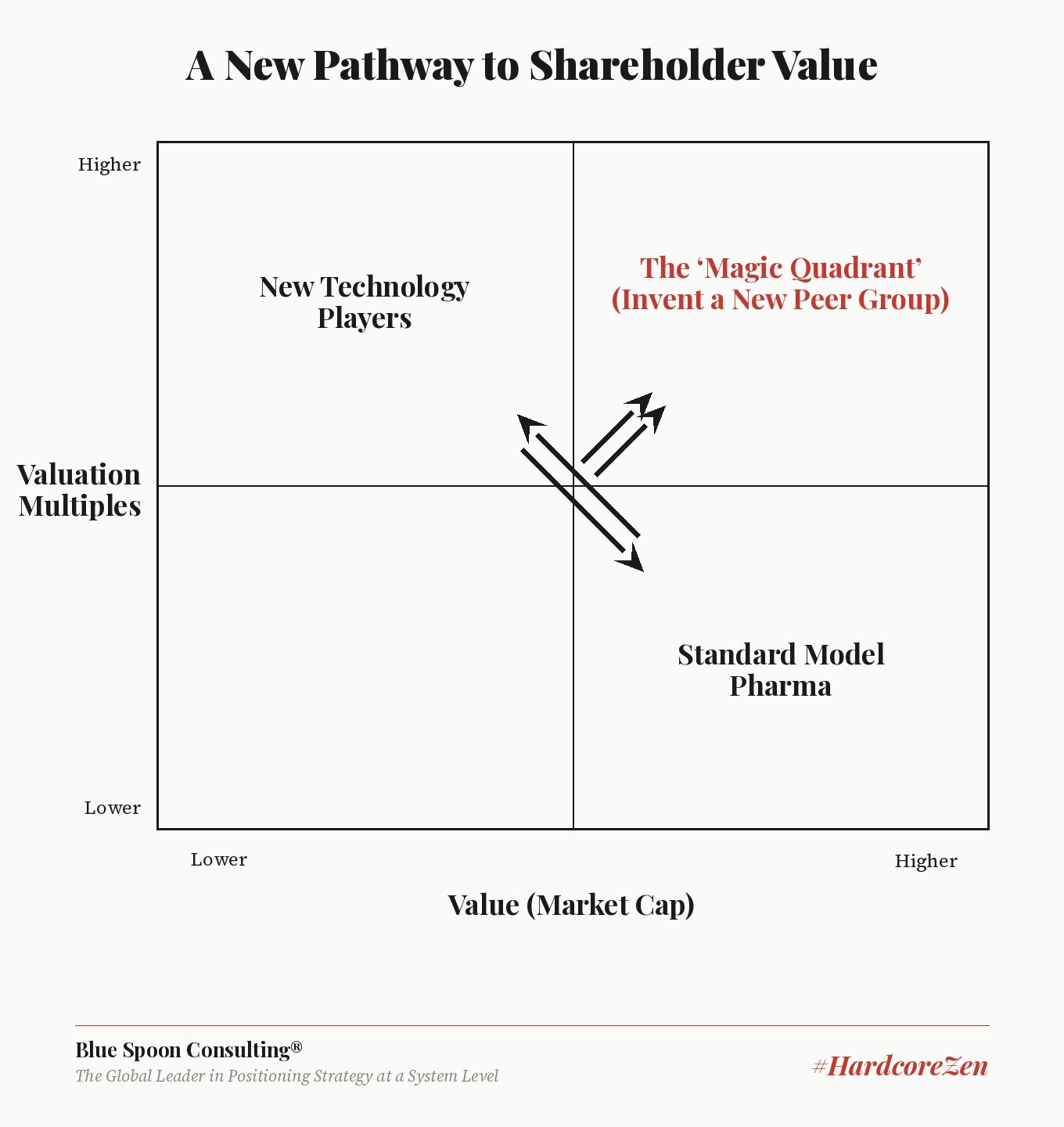

Stuck Working the Wrong Quadrant

Sanofi removed Paul Hudson as chief executive yesterday, thanking him for "valuable contributions" but without giving any reason for his surprise exit.

The working theory making the rounds in analyst calls and reports is that management did not shift the center-of-gravity for big growth and market innovation, meaning Sanofi didn't have an exit strategy from the $17 billion economic system organized to orbit around Dupixent.

Belen Garijo, currently chief executive of Germany's Merck KGaA, will take over in April. "She has a huge task ahead of her," said John Murphy, an analyst at Bloomberg Intelligence, pointing to the need for new products to offset a likely generic hit to Dupixent, which made up 36% of sales last year. "R&D productivity doesn't change overnight, so short of significantly ramping up business development, it's not clear why change won't continue to be gradual."

Murphy's assessment is part of the problem. It is incremental. It is "product productivity" based. It is Standard Model Pharma climbing the existing hill, optimizing the existing machine, stuck searching for a local maxima. It's a 'storyline of value' where Sanofi is being compared to the same peer group, priced by the same narrative, judged by the same industrial logic.

But the market does not reward productivity alone. It also rewards category shift.

The alternative pathway to shareholder value for any drug manufacturer is not about squeezing another 200 basis points out of R&D efficiency, to make the past perform better. It is not about AI as a lab assistant. It is about finding narrative gravity, a new vocabulary to lead big system innovation, vision that moves a business from Standard Model Pharma into a redefined peer set altogether.

Paul Hudson was "excellent at selling dreams", Jean-Louis Peyren of the Fnic-CGT pharmaceutical industry union told AFP. "Instead of having a financier who does more marketing than anything else, we hope that if it's a doctor, she will be more focussed on treatment needs than financials," he said in reference to Garijo.

The irony is that "selling dreams" is the job description for anyone trying to do something genuinely new. And Peyren's Standard Model European view underscores a particularly European epitaph. Mario Draghi's blunt diagnosis of Europe's innovation gap with the United States and China: "We have many ideas, but we struggle to turn them into companies that lead global markets."

You don't escape the Standard Model by doing the Standard Model better.

The question for Sanofi et. al. isn't "how do we replace Dupixent?" It's "how do we stop being the kind of company that's defined by needing to replace Dupixent?"

Now is not the time for anyone to get stuck climbing toward their local maximum. Hudson tried to build something bigger. He tried to cross the valley. He tried to create genuine Galapagos species in an industry that has become a large continent where firmly established ecosystems blur and swamp new adaptations.

And in the end, that path cost him the job.

We're toast if this is what leadership looks like. Not because Hudson was perfect — clinical failures are real, and boards have fiduciary duties. But because the system that ushered him out is the same one that governs the field, the armies of the night that ensures the next CEO will make the same safe choices: these are the analysts, the algorithms, the quarterly rituals, the legal exposure, the consensus narratives clashing in the dark, enforcing conformity without ever quite intending to.

The story here isn't about whether Hudson was right or wrong.

It's about whether any CEO can survive attempting something genuinely new inside a system that has drained away risk tolerance, compressed time into ninety-day increments, and turned long-term imagination into a dismissible liability.

The answer, apparently, is no.

/ jgs

John G. Singer is the founder and Executive Director of Blue Spoon and the author of When Burning Man Comes to Washington: A Field Manual for Riding Chaos. Hardcore Zen is published weekly on Substack.