The Cardiac Borough

The Cardiac Borough is a four-part strategic essay series examining whether the production of cardiometabolic health can become New York City's next economic export engine, replacing the gravitational role Wall Street has played for a century. Published by Blue Spoon Consulting, the series applies ecosystem-centered market strategy and the Hardcore Zen methodology to the question of what happens when healthcare becomes the city's dominant industry.

The complete series, full index, and all charts and figures available for download are at The Cardiac Borough.

For the better part of a century, New York City's economic identity has been inseparable from financial services. Wall Street was not merely an industry; it was the psychic architecture of the city, the thing that gave Manhattan its particular electricity, its ruthless verticality, its unshakable conviction that money — the movement of it, the multiplication of it, the sheer audacity of imagining more of it into existence — was the most sophisticated act a human being could perform.

And for a long time, the city was right. The financial services sector poured hundreds of billions into the regional economy, funded the tax base, kept the restaurants full, the real estate absurd, and the cultural institutions solvent. It was, by any measure, a magnificent run.

But the run is winding down.

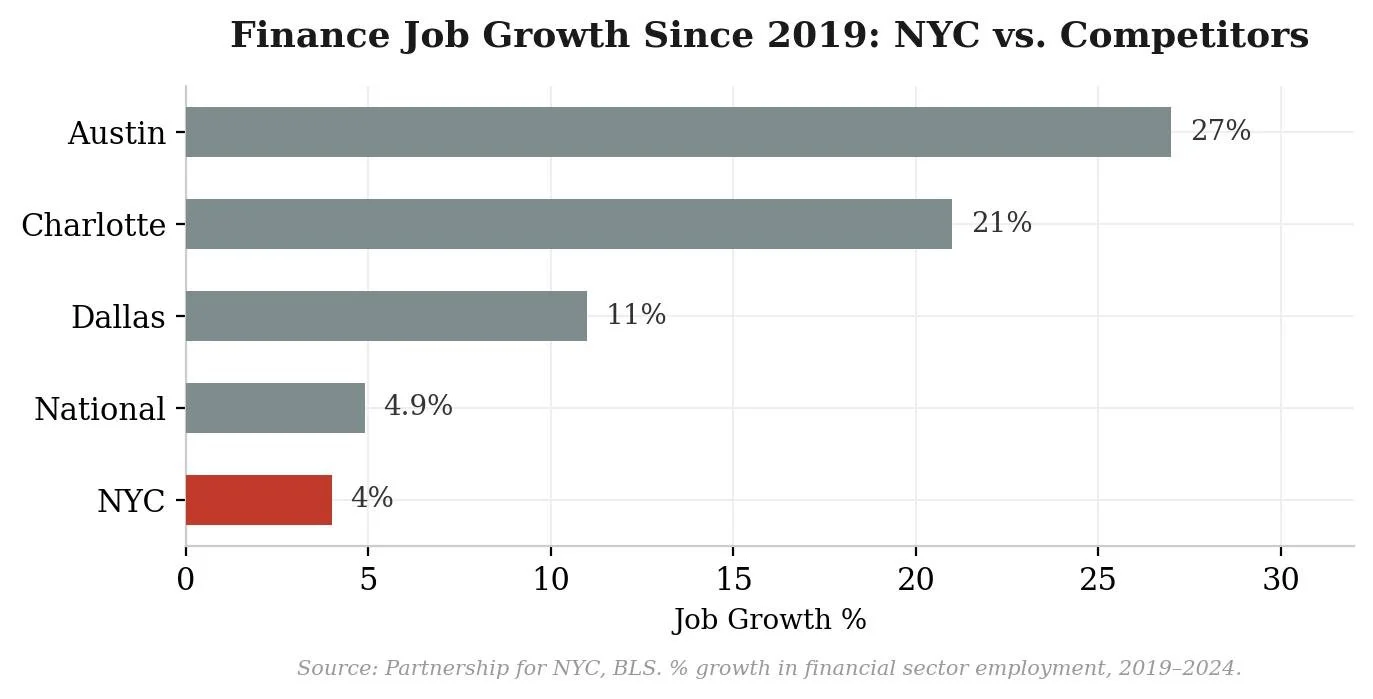

Remote work has distributed the back-office operations of major banks across cheaper geographies. Algorithmic trading has hollowed out the human density of the trading floor. Fintech has democratized functions that once required a physical presence in the canyons of lower Manhattan. But the financial sector is not dying; it's dispersing, which for a city that depends on concentration is almost worse. New York will always have finance, but finance will no longer have the gravitational mass to organize an entire metropolitan economy around itself.

The city now needs a different 'center of gravity', not just another large employer, but a new export engine, a better premise for strategic power and leverage: something New York can sell to the world that pulls outside money into the five boroughs, throws off dense taxable activity, and recreates the multiplier effects finance used to provide. That's what "center of gravity" means here: a sector that doesn't merely circulate local spending, but creates gravitational pull into a new economic orbit. It imports and organizes demand, and then progressively builds a system of secondary markets — real estate, hospitality, professional services, research, education, tourism — around a core product.

Which is the essence of an 'ecosystem-centered market strategy' — not grow one company or sector, but treat a cluster of adjacent markets as a single economic unit, and then deliberately shape the context they operate in. When the surrounding stack of institutions, services, talent pipelines, and contracts all reinforce the same core product, the individual markets stop behaving like separate categories and start functioning as interlocking market sets, each one making the others more valuable. The goal is to build and then swim in a value pool so coherent, and so advantageously organized, that the market doesn't just buy from you. It routes through you. Transactions, talent, standards, data flows, and decision-making start defaulting to your narrative because operating outside it becomes the slower, riskier, lower-trust path.

Whatever replaces finance has to meet four tests simultaneously.

Four Tests for a New Center of Gravity

It has to solve a cold network problem, giving outsiders a reason to show up, plug in, and stay, the way Wall Street's self-reinforcing density of clients, counterparties, talent, and capital once did. It has to produce markets, not merely participate in them, turning a messy domain into something measurable, contractible, and tradable. It has to generate work, real jobs anchored to physical capacity and institutional trust, not just software margins and headcount shrinkage. And it has to do all of this at a moment when the AI narrative keeps trying to wave away the thing that actually matters politically: people.

Jobs are the political substrate. When the "information layer" goes abundant, the backlash arrives fast, and the credibility gap arrives even faster. Verizon CEO Dan Schulman: "I think it's possible that we see 20% to 30% unemployment levels over the next two to five years," and then the dagger framed in The Week the Dreaded AI Jobs Wipeout Got Real, the lead article over the weekend by the Wall Street Journal: "We are at a precipice right now that if you say to your employees there's not gonna be any job disruption, I think you lose all credibility, because all of them get it that there's going to be."

The point isn't whether Schulman's numbers are right. The point is that leaders can't sell a frictionless AI future while the labor market is staring at a cliff.

So the city's next engine has to do more than "grow."

It has to grow in a way that the public can live inside, with marketcrafting in the public interest. This means strategic imagination that builds a sector where unique value is created intentionally, through physical capacity, trusted institutions, and real goods and services, not just software margins and headcount shrinkage. The goal isn't to out-AI an AI economy, an impossible task; it's to build an export that solves a cold-network problem and produces markets: measurable outcomes, repeatable demand, and a thick stack of work that can't be Zoomed and doesn't evaporate when the next productivity wave hits.

Escape to New York

The Cardiac Borough is a thought experiment in what that center of gravity could be.

Not a prediction that it is already forming. Not a forecast. But an exit strategy from a collapsing system the city is now trapped in kinetically: shrinking exports, shrinking tax base, degraded services, accelerated outflow, international tourism down around 20 percent (this matters for a destination like New York — unlike business travelers, international tourists account for a much larger share of spending because they tend to stay longer and spend more).

The claim is that positioning 'the production of cardiometabolic health' as a new economy concept, not just a healthcare agenda, opens space for ambition, big market innovation, a way to frame and approach large-scale 'enterprise transformation' — enormous, structurally sound, market-based, and hiding in plain sight — that no one in city government, in Albany, or in the national conversation is treating as an off ramp.

To keep the argument tight, the essay will run in four parts, each unpacking a different layer of the same question: when care becomes the economy where does value concentrate?

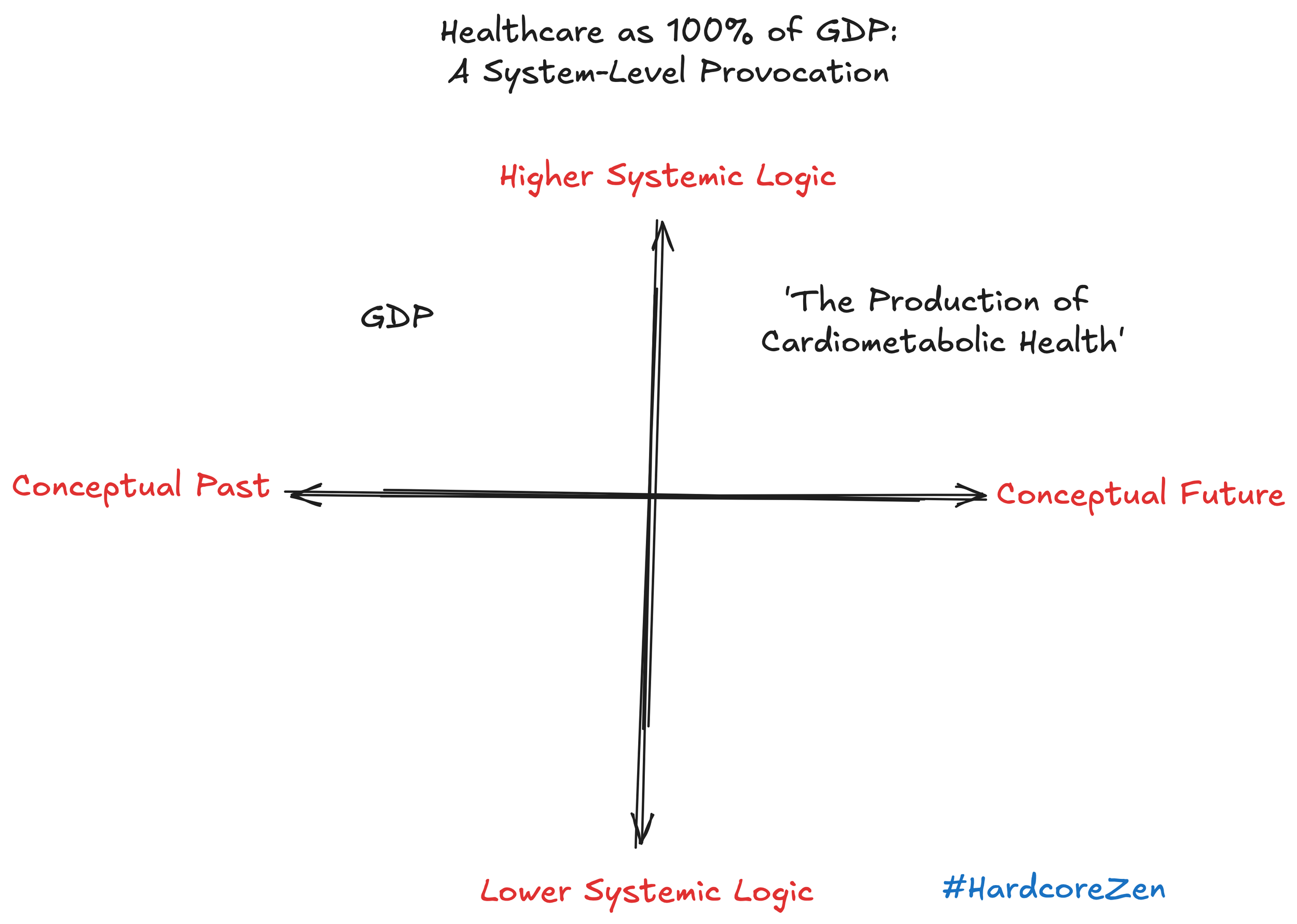

The framework for thinking through questions like this is Hardcore Zen, a positioning methodology developed by Blue Spoon for systems in structural transition. It works by generating system-level provocations: deliberate reframings that force a question out of its conventional coordinates and into the space where the real structural logic lives. The provocation driving this essay is a simple inversion that unsettles everything built on top of it: what happens when you stop thinking of healthcare as a cost center inside GDP and start thinking of GDP as something that happens inside the production of health?

One framing treats care as a line item to be minimized. The other treats it as the organizing principle around which economic life arranges itself.

The entire policy apparatus — every budget negotiation, every reimbursement formula, every political debate, every editorial about "bending the cost curve" and "fixing" healthcare the world over — is built on the first assumption. The Cardiac Borough is built on the second.

Think of The Cardiac Borough as the necessary complement, and strategic counterweight, to the a16z "infinite healthcare" vision that dropped last week.

Where a16z bets on AI turning the information layer of care into an abundant, low-cost utility, their vision still runs into the immovable object: U.S. healthcare is an N-sided market with rules of engagement written and controlled by a small handful of apex species, embedded economic systems like UnitedHealthcare, Express Scripts, Epic, and a few others who decide what gets paid for, what gets routed, and what gets documented.

The Cardiac Borough bets on a different context for competition: physical capacity, material products, brand trust, and the human beings who can reliably deliver outcomes through scarce, real-world goods and services. Here AI is cast as all technology since time immemorial should be: not the lead but an extra, part of the crowd scene in the background, not in the starring role.

It will be published in four parts, with each section dropping weekly over the next four weeks, one lens at a time, moving from macro conditions to demand mechanics to geography to competitive strategy, a single narrative thread building toward the same conclusion from different angles.

After the Anchor Industry frames the macro transition unfolding for New York City: the shift from finance as the signature export to healthcare as the dominant employment base, and why "more healthcare jobs" can either stabilize the city or lock it into managed decline. The difference is narrative configuration: reactive local service versus intentional, exportable production capacity.

A Unique Demand Engine treats GLP-1s as the opening act, and then follows the wake. Behind 'the drug' is the full cardiometabolic health market stack: sensing (CGMs, wearables), prediction (risk engines), optimization (titration, adherence, side-effect management), diagnostics (labs, imaging, biomarkers), interventions (next-gen incretins, combos, devices), nutrition and behavior systems, specialized EMRs, and longitudinal prevention contracts. The point is not that these are separate markets. It's that they're already starting to merge into one integrated complex, a single organism that behaves less like a therapeutic category and more like a production system.

Cities as Platforms makes the geography claim: AI lowers the marginal cost of information work, but trust, patient (family) volume, and institutional density still anchor the highest-value care to physical places. Cities become platforms, people and institutions are out front, AI runs in the background, more like a commoditized technology vendor, and "health production" becomes a new kind of export.

The Next Shift for Pharma turns to the player with the most leverage to reshape the terrain: the pharmaceutical industry, especially the GLP-1 incumbents and challengers. The current competitive script — molecule-vs-molecule, rebate-vs-rebate — is a losing game of incremental technical merits. The claim is that pharma can win through total system leadership: building, branding, and owning the production-of-cardiometabolic-health ecosystem around the drug. The prize isn't just formulary share; it's changing the basis of competition from "best drug at the lowest net price" to "best outcome engine," with the molecule positioned as the keystone to a new industry ecosystem.

As I wrote in Paul Hudson: The Man Who Sold The Stars: The market does not reward productivity alone. It also rewards category shift.

The same could be said for cities.

The Off Ramp

The Cardiac Borough isn't a healthcare idea. It's an economic innovation strategy, one built on a premise that healthcare, treated not as a cost problem or a policy problem but as a city-scale export engine, is the only sector with the structural mass to replace what finance once provided.

Steve Forbes put the danger in characteristically blunt terms last week, asking whether New York Mayor Zohran Mamdani is "putting America's foremost city in irreversible decline."

Forbes noted that the state and the city "have feasted on money coming out of Wall Street, thanks to gains from the stock market boom," but warned that "stocks don't go up forever and, more to the point, banks and financial firms are moving personnel to Texas and elsewhere." He cited the launch of the Texas Stock Exchange as a harbinger, observing that "thanks to technology, location isn't as critical anymore." The City's $127 billion budget, $10 billion larger than Florida's, a state with nearly three times New York City's population, is, in Forbes's view, a government "on steroids" attempting to blackmail Albany into soaking the rich to cover a structural shortfall.

The backdrop for all of this is the new urban physics: high earners can exit the tax base without exiting the economy. California's billionaire-tax chatter is already functioning like a relocation catalyst, and New York's own tax politics are starting to trigger the same reflex. The old bargain, live where you work, pay where you live, is dissolving.

The "lifestyle tax haven" model turns great cities into fly-in nodes: come for the meetings, the deals, the culture; file taxes somewhere else.

For New York City, the 'production of cardiometabolic health' fits the "infinite healthcare" ambition in the only way that matters: it turns 'continuous health engagement' from a cost center into an economic engine, a better concept around which to reorganize and give direction to the thing everyone is looking for worldwide: repeatable demand, market access, measurable outcomes, institutional trust, global inflows, and a thick stack of real infrastructure that throws off local multipliers, even when the wealthy can live elsewhere.

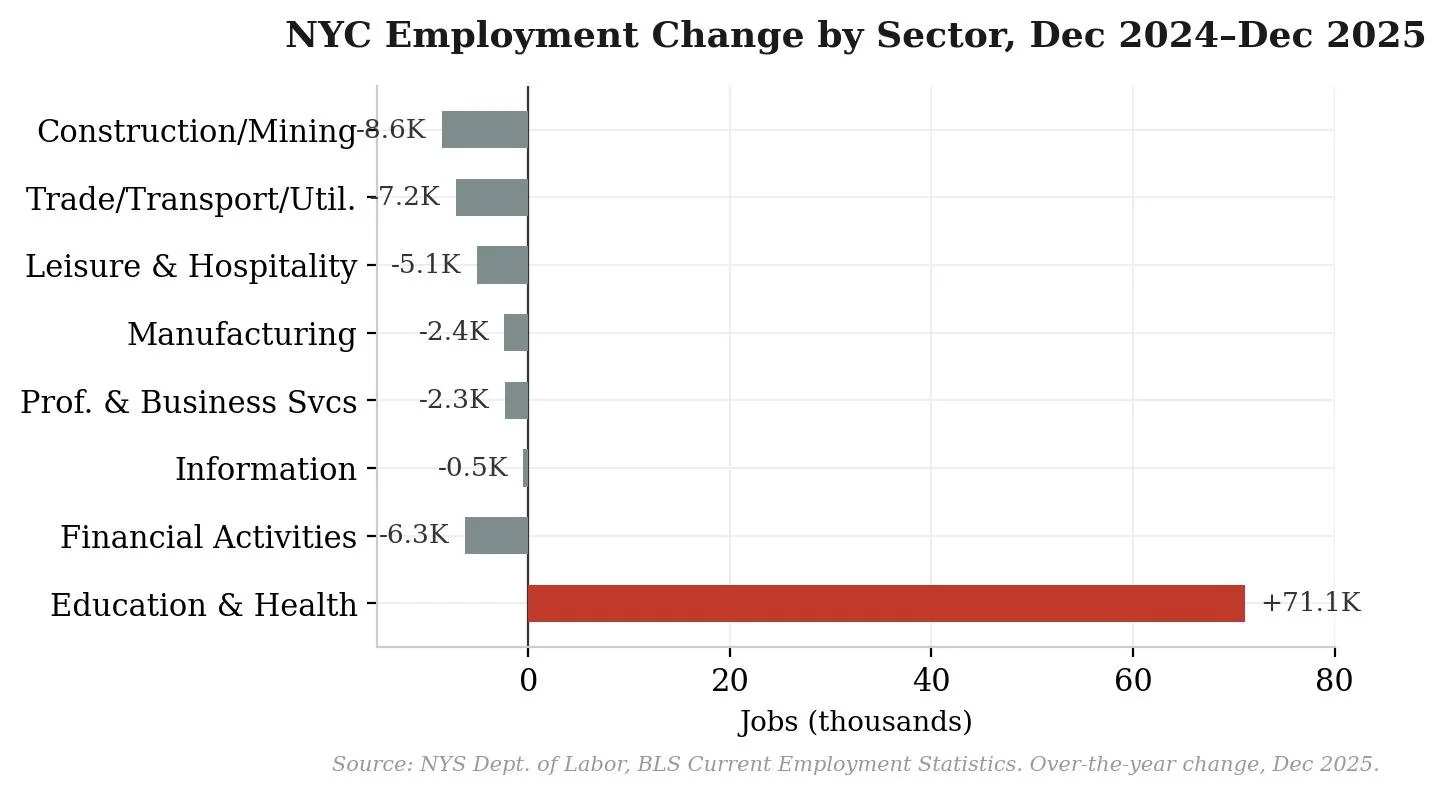

And this isn't a speculative bet on some far-off future. The city is already moving, quietly, mechanically, almost sleep-walking into healthcare as its new anchor industry. If the question is where the puck is going to be, the labor market is drawing the arrow for you:

So here's the cadence for The Cardiac Borough: four parts, four weeks. After The Anchor Industry → A Unique Demand Engine → Cities as Platforms → The Next Shift for Pharma. Each week is one cut at the same underlying question: what does The Big Apple need to become, and what does it need to sell to the world, when "being here" is no longer mandatory?

And then the sharper question underneath it: who picks the next center of gravity, and what happens to the city if nobody does?

/ jgs

John G. Singer is the founder and Executive Director of Blue Spoon and the author of When Burning Man Comes to Washington: A Field Manual for Riding Chaos. Hardcore Zen is published weekly on Substack.