The Cardiac Borough, Part IV: The Cardiometabolic Dividend

The Cardiac Borough is a four-part strategic essay series examining whether the production of cardiometabolic health can replace the gravitational economic role Wall Street has played in New York for a century. Published by Blue Spoon, the series applies ecosystem-centered market strategy — the idea that industries organize around production systems, not products — to the question of what happens when healthcare becomes a city's dominant export.

Part I is here. Part II is here. Part III is here.

Part IV is where the argument becomes a fiscal argument. Parts I through III established what New York has and what it could build. This essay closes the series by asking who pays for it, who owns it, and why the tax fight currently consuming Albany is a symptom of a strategic failure that predates any particular mayor.

There is a fight happening right now in New York City that most observers are framing as a tax fight. Steven Fulop — ex-Marine, ex-mayor of Jersey City, newly installed as president and CEO of the Partnership for New York City, the lobbying and policy organization that represents the city's largest financial, media, real estate, and law firms — is waging a multi-front campaign against Mayor Zohran Mamdani's proposed tax increases on high earners and corporations.

The business community has found a new general.

Fulop took the job in mid-January, waited one week after his third term of Jersey City's mayor ended to start, and sat down with Commercial Observer at his new office in the Financial District at the end of February. The Partnership's member businesses, Fulop told the paper, invest billions of dollars into the city's economy and employ nearly 500,000 people across the five boroughs.

The location for the interview is worth pausing on.

The Financial District — the very geography whose platform premium this series has spent three essays describing, the node in the network whose gravitational pull organized a century of American capitalism — is where the man hired to defend the old economy chose to plant his flag. He is operating, with the unconscious precision of someone who does not know he is making a metaphor, from inside the architecture of the thing that is being displaced.

"Raising taxes in what is already the highest taxed environment in the country simply is not a real solution," he said in a statement within weeks of taking the job. "The city is on a dangerous trajectory." He has since repeated the argument in every forum that will have him, with the relentless discipline of a man who spent twelve years in elected office learning that if you say the same thing enough times in enough rooms, it becomes the frame.

Polls show 62 percent of New Yorkers support the mayor's plan anyway. And while New York Governor Kathy Hochul has (so far) ruled out income tax increases, she has left the door cracked for a corporate surcharge. Moody's has revised its fiscal outlook for the city from stable to negative.

Fulop is not wrong about the danger. He is wrong about what it is.

What Fulop and the Partnership are defending is a revenue model. What Mamdani is proposing is also a revenue model. It is a larger revenue model, one that extracts more from corporations and millionaires who received a massive federal tax cut from Donald Trump last year, but it is a revenue model nonetheless. Both sides are arguing about how to divide what the city already has. Neither is asking where the next thing comes from.

Fulop himself supplied the terms of the hostage negotiation, possibly without intending to: "You don't have to move to Florida anymore. The disparity between New Jersey and New York is going to be so extreme that you'll just have to move two miles." The threat is not hypothetical. It is geographic. It is measured in the distance between the Financial District and the waterfront towers of Jersey City that Fulop spent three terms as mayor helping to build. He knows exactly how easy the move is, because he presided over $1.4 billion in tax roll growth by making it easy.

This final essay in the Cardiac Borough series is about the production model that neither side of the Albany fight has thought to propose. It is about why cardiometabolic health is not merely a clinical category or a public health burden but the terrain on which a city builds its next economy. It is about where the pharmaceutical industry leads, because the pharmaceutical industry, more than any other actor in the system, has the commercial incentive, the scientific infrastructure, the tangible physical products, and the strategic need for exactly the kind of longitudinal, population-scale outcomes data that New York's density can uniquely provide. And it is about a concept that does not yet exist in the vocabulary of urban fiscal policy but will, once someone names it clearly enough to act on: the city as enterprise customer.

Not the city as tax collector. Not the city as regulator. The city as the entity that purchases, on behalf of its population, a continuously produced standard of cardiometabolic health, and that negotiates the terms of that purchase with the pharmaceutical and technology industries as they converge into something neither has been before: a single production ecosystem, drug and data and device and clinical protocol fusing into one economic organism whose output is not a product but a continuously improving standard of metabolic health. The city, in other words, as the buyer that the direct-to-employer shift now underway in healthcare has been building toward all along, operating at a scale that no single corporation, no matter how large its self-insured plan, can match.

The city that figures out how to occupy that role has solved the Fulop problem without ever having to fight the Fulop fight. The tax debate becomes a footnote to a growth story.

Stuck With a Ghost Framework

The Partnership's argument, stripped of its courtesies, runs as follows: New York's tax burden is already near the limit of what its business class will absorb. The city's top combined corporate rate is 17.44 percent. Mamdani's proposal would push it toward 22.48 percent. Push past the limit and the productive capital relocates to friendlier jurisdictions.

The city loses the tax base it was trying to expand. Everyone is worse off.

Mamdani's argument, stripped of its populism, runs the same way in reverse: the wealthy received a massive federal tax cut and can afford to pay more; the corporations headquartered here generate profits that depend on the city's infrastructure, its workforce, its density; asking them to contribute a larger share is not punishment but arithmetic. The $5.4 billion budget gap is real. The services that close it are real. The people who depend on those services, the teachers and the transit workers and the home health aides earning $40,000 a year managing someone else's chronic disease, are real.

Both arguments are sound within their own logic. The trouble is the logic itself.

Both sides are operating inside a ghost framework: a mental model that accurately described a previous system and continues to feel authoritative long after the system it described has moved on. The BCG Growth-Share Matrix, the tool the Partnership's worldview implicitly relies on, was designed in the 1970s for a world where markets are stable, industries are bounded, and the job of management is allocation, not creation. Mamdani's redistributive model, for all its moral clarity, accepts the same premise from the opposite direction: that the pie is fixed and the only question is how to cut it.

The ghost framework traps both sides.

It tells the Partnership that the only way to grow is to keep rates low enough that existing capital stays. It tells the mayor that the only way to fund services is to extract more from the capital that is here. Neither framework has a theory of new economic mass. Neither asks what New York could produce that does not yet exist, what industry the city could organize around itself that would generate revenue the way Wall Street generated revenue for a century: not by taxing the activity, but by being the infrastructure the activity cannot function without.

Last week offered two illustrations of what a ghost framework produces when it encounters a world it was not built to describe:

On Wednesday, Mark Zuckerberg's Meta announced it would shut down Horizon Worlds, the virtual reality platform at the center of the metaverse vision he renamed his entire company to pursue. Reality Labs has accumulated roughly $80 billion in losses since 2020. The metaverse was supposed to be the next platform, the thing after the smartphone, the infrastructure through which a billion people would work and socialize. It attracted fewer than 200,000 monthly active users. Zuckerberg is now pivoting to AI, training a CEO agent to help him do his own job, and spending hundreds of billions on data centers. But he still needs to feed those data centers, as Part III of this series argued, with something the internet cannot provide: continuous, longitudinal, high-frequency biological signal from real human bodies living real metabolic lives. The cardiometabolic record is that signal. Zuckerberg spent $80 billion building a virtual world nobody wanted to live in. The world people actually live in, the one generating the biological data his AI models will eventually need, is right here. Zuckerberg is not the platform builder of the next economy. He is a customer of it.

On Thursday, the Justice Department filed an antitrust lawsuit against NewYork-Presbyterian, the largest and most powerful hospital system in Manhattan, alleging that it used its market dominance to impose contract restrictions that blocked insurers from offering budget-conscious health plans and prevented employers and unions from steering patients to lower-cost competitors. The DOJ's complaint describes a hospital system that negotiates on an all-or-nothing basis, insulating itself from price competition while charging more than NYU Langone and Mount Sinai for comparable care. This is what the ghost framework looks like when it is applied not just to city fiscal policy but to hospital strategy: a dominant institution using its position to extract value from the existing system rather than building the production infrastructure that would make itself indispensable.

The complaint had originated, in part, with a union grievance from Local 32BJ, the workers whose members clean the lobbies of the buildings on Wall Street where the Partnership for New York City holds its dinners. New York-Presbyterian is not a bad actor in this story. It is a rational one — rational within a framework that never asked what a hospital system should produce, only how completely it could dominate what already existed. The institution that organizes the cardiometabolic borough does not need to fear the Justice Department. It is the infrastructure the Justice Department would have to protect.

New York City, in 2026, sits at the intersection of the two most powerful ecosystem-design opportunities in the global health economy: the cardiometabolic disease burden, which is the largest single driver of preventable mortality and economic loss in the United States, and the direct-to-employer shift in pharmaceutical and health services delivery, which is quietly dismantling the Big PBM and insurance industry's stranglehold on market access to innovation, the production of health and rebuilding US healthcare with an entirely different economic logic.

The question is not whether New York can tax its way to solvency. The question is whether New York can position itself as the keystone of what comes next, and in doing so, generate a revenue stream that no corporation can threaten to take to New Jersey or Florida or Texas.

The home health aide in the South Bronx earning $17 an hour is not a bystander in this argument. She is its central exhibit. In the Partnership's framework, her wage is a labor market outcome, determined by supply and demand, and the best the city can do is keep the economy healthy enough that opportunities eventually trickle toward her. In Mamdani's framework, her wage is a justice problem, and the solution is redistribution from those who have more. In neither framework is she recognized for what Part II of this series argued she actually is: a node in a production system whose economic value, if the system were properly designed, would be orders of magnitude greater than what she is currently paid to do.

The ghost framework cannot see her. The production model can.

Active Bypass

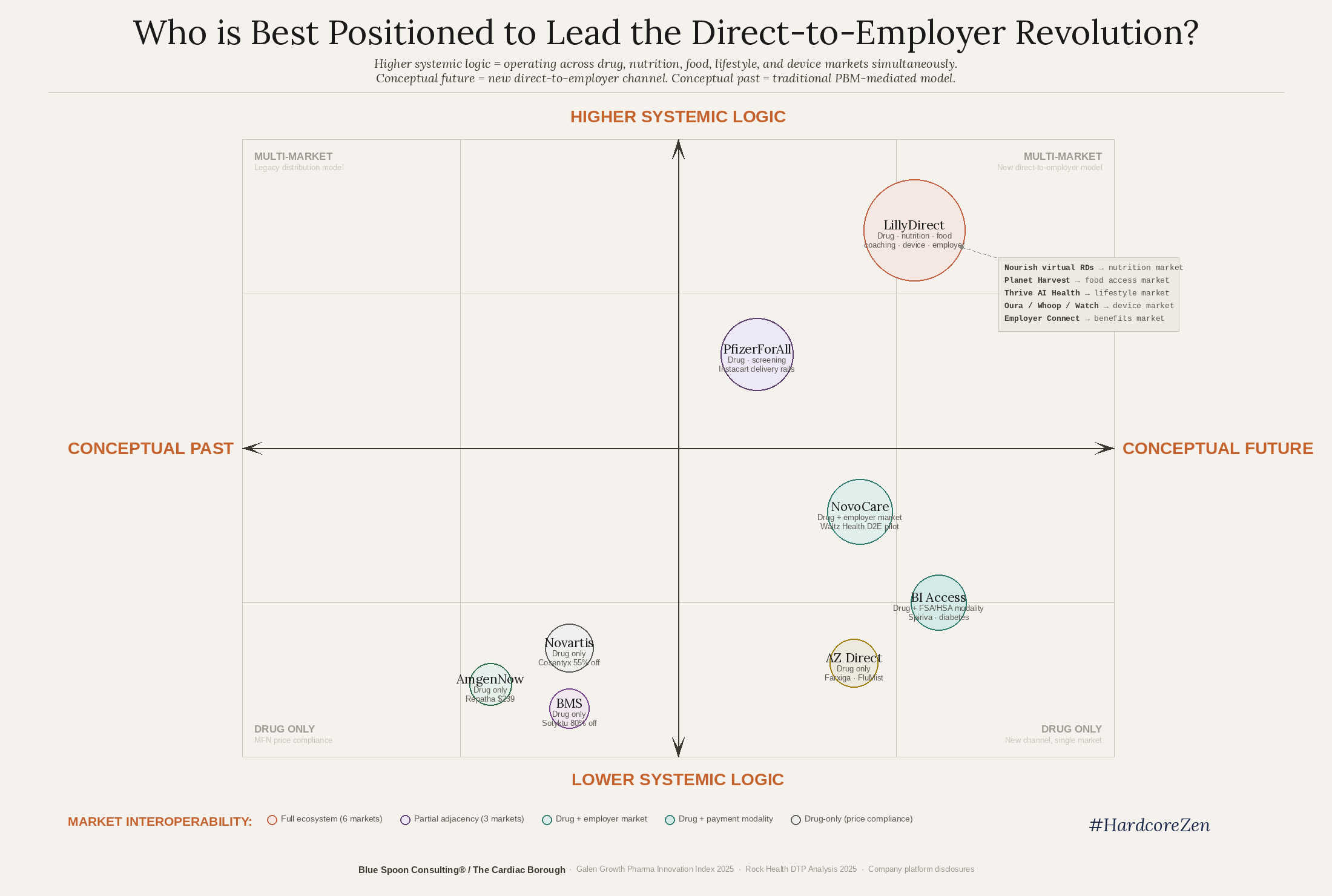

Something has been happening in the pharmaceutical and health services industry that most analysts and journalists are still reading with the wrong lens. They see it as a collection of separate moves: Amazon acquiring One Medical and expanding clinics into new markets. Eli Lilly launching LillyDirect, a platform for selling drugs straight to patients, which Pfizer then followed, which Mark Cuban then praised as a template for how manufacturers can better serve patients, which Trump then capped by sending letters to 17 pharma CEOs telling them, in effect, that none of it was moving fast enough.

Each move is reported as a discrete corporate strategy. What is not reported is that these moves are converging into a single structural displacement. Large employers are building their own primary care and chronic disease management infrastructure, bypassing traditional insurance altogether.

The thing being displaced is a Big PBM market and the Big EBC market, which operates as a single organism: the pharmacy benefit managers, the employer benefits consultants, the insurance formularies, and the claims adjudication machinery that together constitute the embedded economic system through which the value of health has been defined, controlled, priced, and rationed for decades.

Amazon is not a retailer that added a health clinic.

Amazon is an infrastructural technology, a system-level actor that intuitively understands how to create gravitational pull into a better care and service infrastructure. LillyDirect is not a distribution channel. It is a proof of concept for an entire industry going direct to employers.

Part II of this series documented the most telling evidence of this shift: when Walmart needed complex surgery for 1.1 million employees in its health plan, it built its own network of centers of excellence — Mayo Clinic in Rochester, Cleveland Clinic in Cleveland, Geisinger in Danville, Virginia Mason in Seattle. When Boeing needed cardiac care, it contracted directly with Cleveland Clinic, fixed price, full travel included. When Lowe's, PepsiCo, and General Electric followed the same logic, the pattern ran through every region of the country. Not one New York City hospital system appeared on any of these lists.

The pattern is worse than absence. It is active bypass.

JPMorgan Chase, headquartered on Park Avenue, created Morgan Health, an entire business unit dedicated to fixing employer-sponsored healthcare for its workforce. Where did it build its first advanced primary care infrastructure? Columbus, Ohio. Where did it invest in fertility services through Kindbody? Columbus, Ohio. The largest bank in America, sitting in the middle of the largest concentration of hospital systems in the country, looked at what those systems were offering and built its alternative eight hundred miles away.

Meanwhile, Cleveland Clinic solved for New York by not starting in New York: it formed an alliance with Northwell Health to provide direct-to-employer cardiac care in the New York market, because no New York City hospital system was offering what employers wanted. Cleveland Clinic had to reach into the city from Ohio to fill a gap that fifteen Manhattan hospital systems, collectively generating tens of billions in annual revenue, had not thought to fill themselves.

The implication for pharmaceutical companies is profound and has not yet been fully priced into strategy. For decades, the drug industry sold to a market mediated by pharmacy benefit managers, insurance formularies, and provider prescribing behavior. The customer was not the patient. The customer was not even the employer. The customer was the administrator of the system that stood between the drug and the person who needed it.

That legacy 'system of record' is cracking.

The Mount Sinai–Anthem contract failure documented in Part II, which threw thousands of patients out of network, was not an anomaly. It was what happens when the existing infrastructure, built to adjudicate episodes and manage the cost of what went wrong, encounters a market that wants something the infrastructure has no architecture to provide: the continuous management of what could go right.

What the direct-to-employer shift creates is a new buyer: a large, sophisticated, self-insured corporation that is not primarily interested in "drug spend and trend." It is interested in employee health outcomes measured against its own operational and financial metrics: absenteeism, disability claims, productivity, retention. For cardiometabolic conditions, which are the leading driver of all of those metrics, this buyer is willing to pay for a system that works. Not a drug. A system of which drug is a part.

And here is the fact that connects the tax fight in Albany to the cardiometabolic economy being built everywhere except New York: New York City is home to the largest concentration of those buyers on earth. The Fortune 500 companies headquartered in the five boroughs, the financial services firms whose self-insured plans cover millions of workers nationally, the municipal and union health funds whose collectively bargained benefits represent what Part III called the single largest organized pool of healthcare purchasing power in the country — they are all here. The buyers are here.

What is missing is the system they are trying to buy. And as long as what the city offers those buyers is a tax rate rather than a production system, Fulop's argument wins by default.

Biological, Not Behavioral

A platform, at sufficient density, stops facilitating transactions and starts self-generating markets, producing new categories of value that did not exist before the network existed and cannot be specified in advance by any of its participants.

Amazon now makes more money enabling other people's commerce than selling things itself. The platform ate the transaction and became a $717 billion/year economy. The App Store did not distribute software. It produced a new kind of developer, a new commercial logic, a new consumer behavior that Apple and its million developers discovered together as a byproduct of the interaction itself. What Amazon and Apple both learned is that the skill was never the platform. The skill was frontier management: governing the edge of what nobody had specified yet.

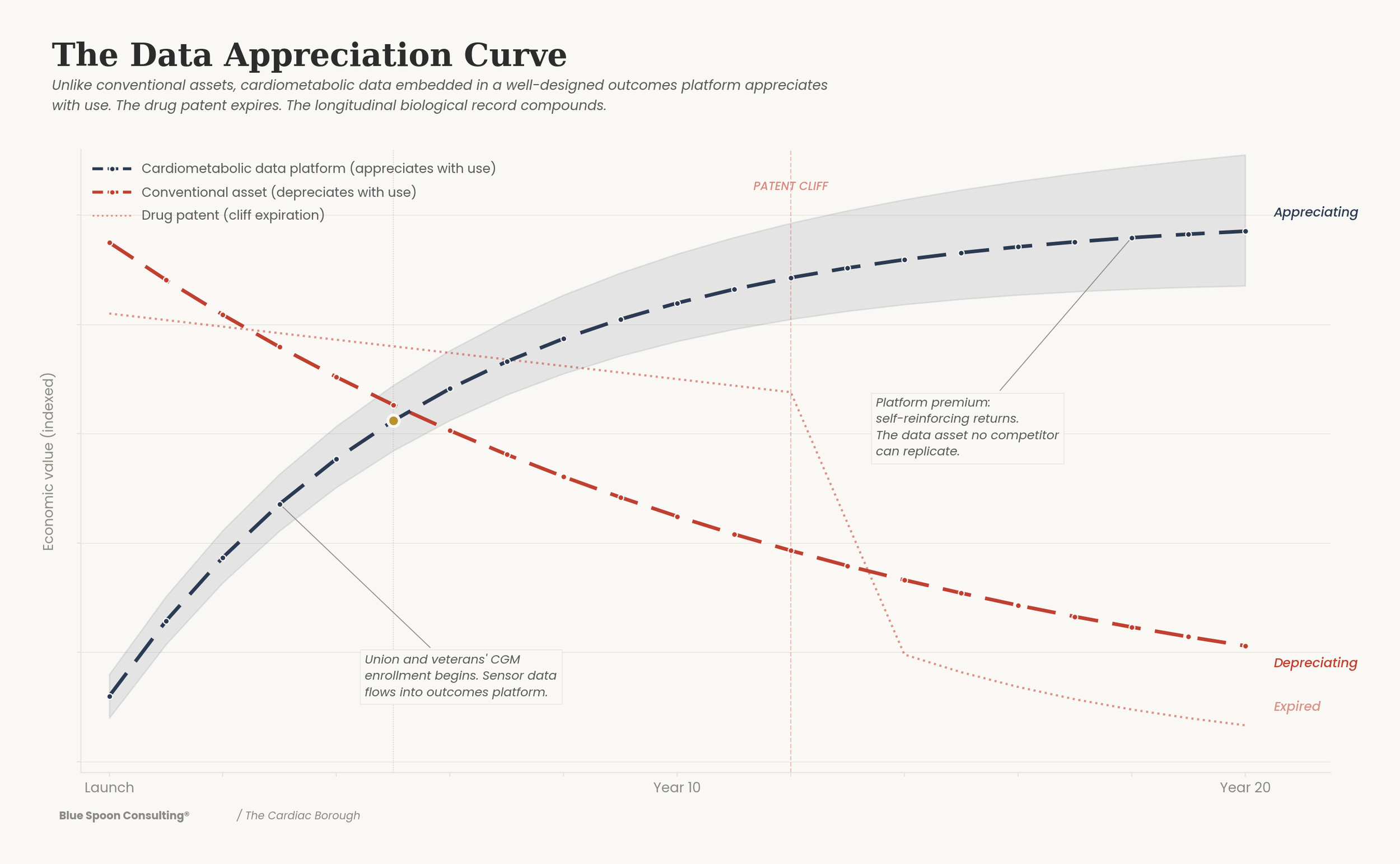

The cardiometabolic platform crosses that threshold because the data it generates is not behavioral. It is biological.

Meta's empire is a $1.5 trillion enterprise built on what people say and do with their attention, via clicks, shares, reactions, the behavioral signal of engagement. Last week, a Los Angeles jury found that empire negligent in the design of its platforms, concluding that Instagram was deliberately built to be addictive and that Meta knew it and failed to protect its youngest users. The plaintiff's attorneys reached for Big Tobacco. The liability exposure now facing behavioral data platforms — 2,000 pending suits, a federal trial this summer, the Section 230 shield cracking at its seams — is structural, not incidental.

It is the bill that arrives when the asset you have been monetizing turns out to be the attention of children you were supposed to protect.

The signal the cardiometabolic platform generates does not have that problem. It is the body's continuous, unsolicited, uneditable account of what is actually happening inside it, produced by consenting adults whose health outcomes improve because the platform exists, whose data generates knowledge that extends lives rather than shortens attention spans. It cannot be scraped. It cannot be modeled from a corpus. It must be produced by real bodies, in real time, in a real production system.

What the data appreciation curve above is measuring is this: not the value of individual records, but the value of the system those records constitute. Look at the curve's inflection point — the moment the platform stops accumulating data and starts generating intelligence that none of its participants could produce alone. That intelligence is densest at the intersections the curve cannot show directly: where cardiometabolic disease meets fertility outcomes, where GLP-1 response varies across ancestry groups, where the construction worker's glucose trajectory after a night shift diverges from the home health aide's in ways that have never been measured because neither population has ever been continuously monitored at scale. New York's population generates those intersections by its nature. No clinical trial can manufacture them.

The city's density, which accountants treat as a cost to be managed, is the mechanism of value creation. The overcrowding is the asset.

What is currently being harvested piecemeal by individual health systems competing for share of a market fragment could, in aggregate, become a self-generating system of markets, a new business ecosystem that produces new questions, new hypotheses, new commercial opportunities around cardiometabolic literacy faster than any single institution can capture them. And when Meta or Amazon or the sovereign wealth fund manager in Abu Dhabi — or the pharmaceutical company trying to prove its GLP-1 successor works differently across 23 distinct metabolic phenotypes its Phase III trial never captured — when any of them needs that biological signal at scale, they become customers of New York City in the only sense that matters: they have no alternative source.

The Prior Question

Alaska taxes the extraction of a natural resource — oil — and distributes a portion of the proceeds directly to residents as a permanent fund dividend.

The economic logic is straightforward: the resource belongs to the people; its extraction generates value that should accrue to them; the mechanism is a dedicated fund whose earnings are distributed annually rather than absorbed into general revenue.

This is not a metaphor deployed for rhetorical convenience. It is the argument the entire series has been building toward, and it is meant literally.

Part I established that the cardiometabolic drug market projected to exceed $250 billion by the early 2030s, plus a $76 billion global medical tourism industry growing at double digits, plus the essentially infinite addressable population willing to spend extraordinary sums to remain metabolically healthy, constitute an industrial opportunity of a scale the city has not seen since finance rewrote the rules of American capitalism in the 1980s. Part II established that the demand curves in this market are among the most inelastic in the economy, because the alternative to metabolic health is not a competitor product, it is the loss of something irreplaceable: a mind, a child, a parent who still recognizes you. Part III established that the union and veteran's health enrollment mechanism, the longitudinal biological record, and the sensor infrastructure create a data asset whose value appreciates continuously and cannot be replicated by any competitor geography.

What Part IV adds is the fiscal architecture.

A population of 8.3 million human beings whose health data, aggregated across clinical encounters, continuous sensor readings, and social determinants, constitutes one of the most valuable scientific and commercial assets in the global health economy. Pharmaceutical companies, insurance companies, technology companies, data brokers, digital health start-ups, and research institutions are already extracting value from this resource — through clinical trials, through actuarial modeling, through genomic research, through real-world evidence studies. They are doing so largely without compensating the city, its residents, or its healthcare institutions for the value of the raw material.

This month, Novartis settled a lawsuit brought by the estate of Henrietta Lacks, the Black tobacco farmer whose cervical cancer cells were taken without her knowledge at Johns Hopkins in 1951, reproduced in laboratories for seventy-five years, and used to develop drugs Novartis, and many others, sell today. She was buried in an unmarked grave. Her family received nothing. The settlement terms are confidential. The principle is not: a body whose biological material generates commercial value has a claim on that value, and the absence of an architecture to make that claim does not extinguish it, it defers the reckoning until someone else designs the terms. And last week, a breast cancer patient filed a class-action lawsuit also against Novartis, alleging it harvested her health data through tracking pixels on its drug websites and transmitted it to Google and other third parties without her consent.

She had visited to understand her treatment. She left with targeted advertisements for products related to her diagnosis.

Health data on the black market fetches $250 per record, forty-six times the value of a stolen credit card. The lawsuit has a hundred thousand potential plaintiffs. It is one case in what is becoming a pattern: the biological signal generated by a person living her life is worth something to someone, that someone has built an architecture to capture it and a market exists to sell it, and the person whose body produced it was not part of the design.

This is the structural condition the Cardiac Borough series has been circling for four essays. It is not a pharmaceutical industry problem. It is a value extraction problem, the same problem that makes New York's fiscal model perpetually precarious, the same problem Fulop is trying to solve by keeping tax rates low enough that the big investors don't leave, the same problem Mamdani is trying to solve by taxing the extraction harder before it does.

Neither of them is proposing to change who owns the architecture. Neither of them is asking the prior question: what if the city built one of its own?

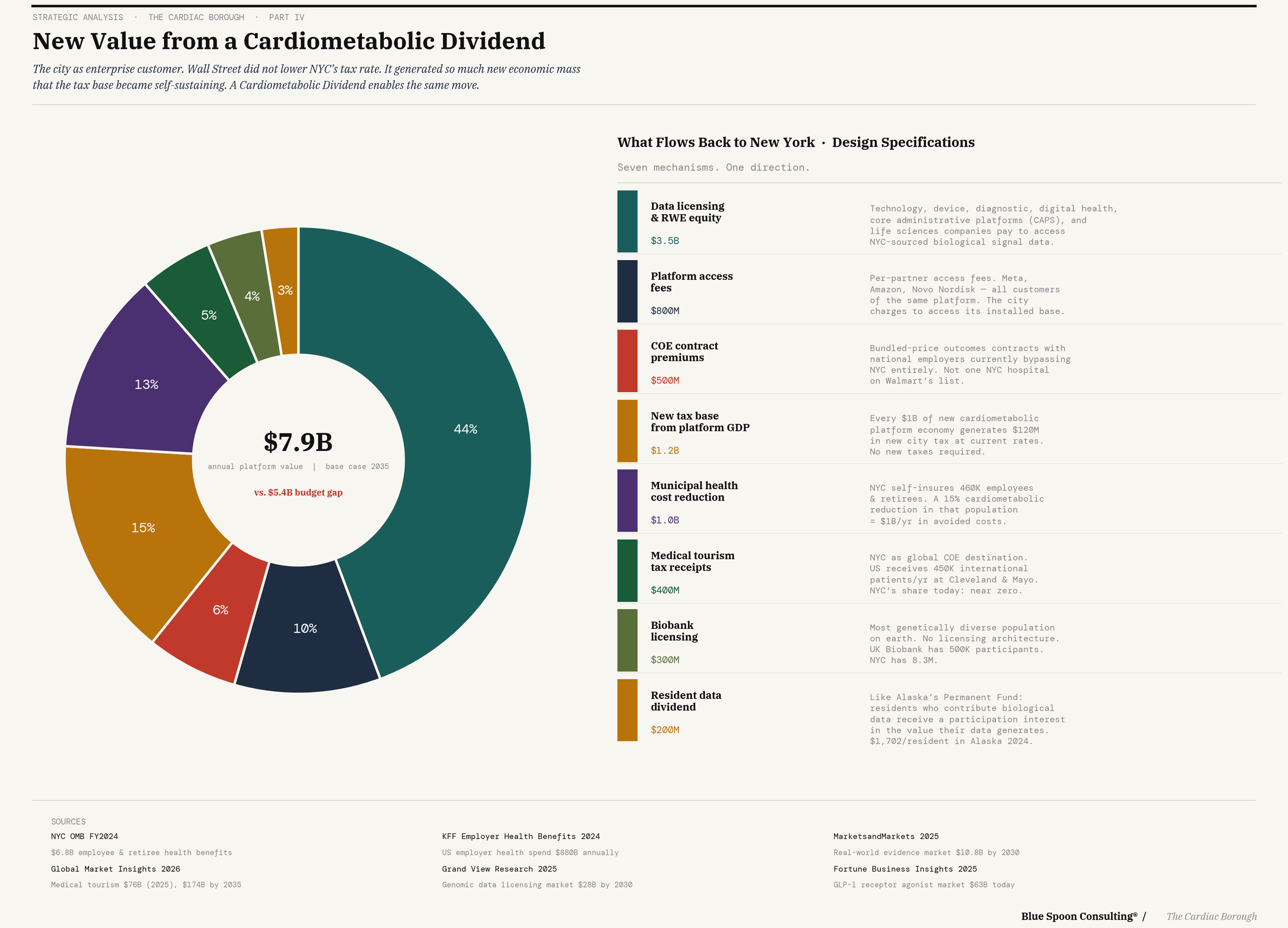

A Cardiometabolic Dividend is that architecture.

Not a tax. Not a lawsuit. A data participation agreement — a structured arrangement through which the city, acting as the convening authority and mediator for a cardiometabolic ecosystem, licenses access to aggregated, de-identified outcomes data to partners in exchange for a participation interest in the commercial value those partners generate from that data. Not a royalty. An equity stake. The city becomes a participant in the upside of the innovations its population enables — the arrangement Henrietta Lacks never had, formalized in advance, managed as a public asset, on terms the city sets rather than litigates.

Walmart captured something structurally similar when it negotiated bundled payments directly with Cleveland Clinic and Mayo — not a discount on procedures, but a fixed price for an outcome, which made the hospital a co-investor in keeping Walmart's workers healthy rather than a fee-for-service vendor paid more when they got sicker. The hospital's incentive and the employer's incentive became the same incentive.

That is what value alignment looks like when it is designed rather than litigated.

The sequence Part III described still holds: union and veteran's health enrollment generates the sensor data and the clinical protocols; the protocols generate the outcomes evidence; the evidence generates the COE contracts; the contracts generate the partnerships; the partnerships generate the data licensing revenue. Each layer earns the right to build the next one. The enrollment is the platform in its first form. The Dividend is the platform in its mature form, the moment the self-generating market begins returning value to the city.

This is how you solve the Fulop problem. Not by taxing what already exists. By building the architecture that determines, from the beginning, who captures what the city produces, and by getting there before the courts design it for you, one case at a time, on terms nobody controls.

New York, properly positioned, is that player. Not because it is the biggest pharmaceutical market or the richest employer or the most advanced research center — though it is all of these — but because a city is the only 'enterprise customer' that can legitimately convene all the others around a shared vision of cardiometabolic health production as an economic export strategy.

The City as Enterprise Customer

The Mamdani tax fight, read in this light, is a symptom of a deeper strategic failure that predates any particular mayor or administration. New York has been, for decades, a world-class destination for economic activity — finance, media, real estate, technology — without developing a theory of how to capture durable value from that activity as a city. The result is perpetual fiscal precarity punctuated by boom-and-bust cycles driven by industries that have no particular loyalty to New York and every incentive to leave when the price is right.

Healthcare is different from every other industry New York has hosted. Healthcare cannot be fully offshored. Clinical trials require patients. Outcomes data requires populations. The production of health requires proximity to the people whose health is being produced.

New York's cardiometabolic patient population is not going to relocate to Miami because the tax rate is lower. The construction worker in the Bronx, whose continuous glucose readings are feeding the platform's predictive models, is not going to move to Jersey City. The 32BJ member whose metabolic record accumulates continuously because the Health Fund carries across job changes is not going to interrupt that record because a hedge fund manager on Park Avenue decided the pass-through entity tax credit was insufficient.

The asset stays. The question is who captures the value it generates.

The answer, in the Cardiac Borough frame, is New York — not through redistribution, but through production. Not by taxing the value that corporations extract from the city, but by becoming the irreplaceable infrastructure through which that value is created in the first place. The platform premium cannot be extracted from an entity that is the platform.

This is the new economy strategy that the Cardiac Borough has been crafting across four essays and approximately 20,000 words. Not a healthcare hub. Not a biotech cluster. Not another innovation district whose economic contribution is measured in square feet of lab space. A different system of markets organized around the production of cardiometabolic health as a deliberate export strategy, with New York City as its keystone, its governance layer, and its primary beneficiary.

The Cardiometabolic Dividend is not a metaphor.

It is a design specification for a new economy model, one that changes the terrain on which the Albany fight takes place, because it is generating new value rather than redistributing existing value. One that turns the city's greatest apparent liability into its greatest asset: a biological data resource so deep, so diverse, and so continuously appreciating that entire industries will pay for the privilege of building on top of it.

/ jgs

John G. Singer is the founder and Executive Director of Blue Spoon and the author of When Burning Man Comes to Washington: A Field Manual for Riding Chaos. Hardcore Zen is published weekly on Substack.